Went out to the Bay Area for my niece's wedding. Great trip, had fun, glad to be home given the price of houses and a wee bit of overcrowding. Seems that I am not the only one glad to be out as outlined in this article at MarketMinder.com. Enjoy--if you can.

California Hates the Poor

10/5/2007 |

California hates the poor. At least the Golden State certainly seems to act that way, given the way it treats its lower-income residents.

But wait—isn’t California known as one of the most socially progressive states, spending billions of dollars on social programs and public assistance for low-income residents each year? Indeed! Yet Californian legislators uphold a policy choking off precious dollars that could go to residents needing it most. That wacky policy is the Golden State’s tax structure.

California boasts the most punitive state income tax system in the entire Union. (Not so fast New Jersey, Hawaii, Iowa, and Oregon! Though you’re all nearly as bad.) With so much wealth in the state, you might not feel much immediate sympathy for those paying the lion’s share of the state taxes. After all, California’s got Hollywood movie stars, celebutants, and Dot-Com-mega-billionaires! Make them pay! Folks tend to forget California has millions of souls—the vast majority are Average Joes.

Let’s examine the current tax structure. California income taxes kick in at a modest 1% rate for annual income up to $6,622. Not too bad—$6,622 seems a small amount to hit up for income tax, but 1% isn’t that much. But, California’s highest tax bracket of 9.3% (the highest in the nation) begins at the affluent, wallet-busting, Bentley-driving sum of $43,468.

I’ll repeat that. California imposes the nation’s highest state income tax level of 9.3% on residents earning more than $43,468. Some perspective: In 2004, the US Census reported California’s median income was $51,185—higher than America’s median income of $44,648. Translation: If you’re “middle class,” California wants 9.3% of your income. It’s a shakedown for your lunch money.

Meanwhile, nearby states Washington, Nevada, and Texas charge no state income tax at all. Arizona starts its highest tax bracket at $150,000 where residents pay 4.57%—less than half California’s top rate. It’s hardly surprising these states are some of America’s fastest growing states. In 2006, Arizona’s and Nevada’s populations swelled over 4 times faster than California’s.

If you’re a Californian with a nice retirement savings, where would you retire? California wants a hefty portion of your retirement income every year, whereas nearby Washington and Nevada want none. Add to the equation the far lower cost of living in those states, and relocating seems like a no brainer. So, folks leave and California ends up with none of their income, property, or sales tax revenue.

Those poor souls remaining in California end up with less money to fund public schools, build new roads, pay for social programs and so on. All thanks to politicians ignoring fundamental economic principles and placing too heavy a burden on its working residents and businesses.

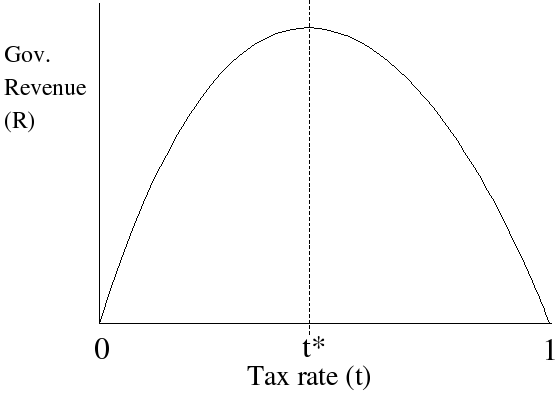

When a state places too heavy a tax burden on its citizens or businesses, the government stifles consumer spending, business investment, and actually ends up collecting far less tax revenue. A government can maximize its tax revenue at an optimal point. Tax too much and folks don’t see much of a reason to get out of bed in the morning. Mrs. Entrepreneur fails to see the upside in launching her cutting-edge new business idea. Less business activity means less tax revenue. The Laffer Curve (shown here

http://upload.wikimedia.org/wikipedia/commons/4/47/Laffer_Curve.png) demonstrates the concept.

If prohibitive taxation makes a difference between US states, one could also apply the concept to countries. When a nation imposes high hurdles for new business development and wealth creation, the prospect of strong economic growth becomes increasingly remote. Conversely, if a country slashes corporate tax rates to spur economic activity, all other factors remaining constant, that’s bullish for growth.

Take Ireland for example. The Emerald Isle slashed its corporate tax rate to 12.5%—one of the lowest rates in the developed world.

Selected Corporate Tax Rates by Country

Ireland 12.5%

Netherlands 25.5%

United Kingdom 30.0%

China 33.0%

Belgium 33.9%

France 34.4%

Germany 38.6%

USA 39.5%

Japan 39.5%

Much to the chagrin of France and other EU heavyweights, economic growth in Ireland is soaring! After all, entrepreneurs and existing businesses only need two very simple elements to justify a venture: profit and human capital. Ireland has an educated, English-speaking work force and a corporate tax rate low enough to entice entrepreneurs from around the globe. Ireland will likely attract business activity, people, and tax revenue other countries will miss out on. It shouldn’t be much surprise, then, that Irish GDP growth is expected to more than double the EU’s average. Erin go bragh!

Eastern Bloc countries are also joining the low-tax party. Estonia, Latvia, Russia, Ukraine, Slovakia, Romania, Georgia, and Macedonia all successfully introduced low flat tax structures in recent years. These moves now pressure Western European countries to either become more competitive with their business climates or face a hemorrhaging economic growth towards their neighbors with cheap labor and more welcoming tax structures.

With one of the largest gross domestic products in the world, one could only dream of the economic boom resulting from slashed California tax rates (not to mention falling federal tax rates). With the Irelands and Nevadas out there, Uncle Sam and the Golden State better act fast. Their poor depend on it.

{kind=link}